A blockchain is a distributed database or ledger shared across a computer network's nodes. They are best known for their crucial role in cryptocurrency systems, maintaining a secure and decentralized record of transactions, but they are not limited to cryptocurrency uses. Blockchains can be used to make data in any industry immutable meaning it cannot be altered.

Since a block can’t be changed, the only trust needed is at the point where a user or program enters data. This reduces the need for trusted third parties, such as auditors or other humans, who add costs and can make mistakes.

Key Takeaways

- Blockchain is a type of shared database that differs from a typical database in the way it stores information; blockchains store data in blocks linked together via cryptography.

- Different types of information can be stored on a blockchain, but the most common use has been as a transaction ledger.

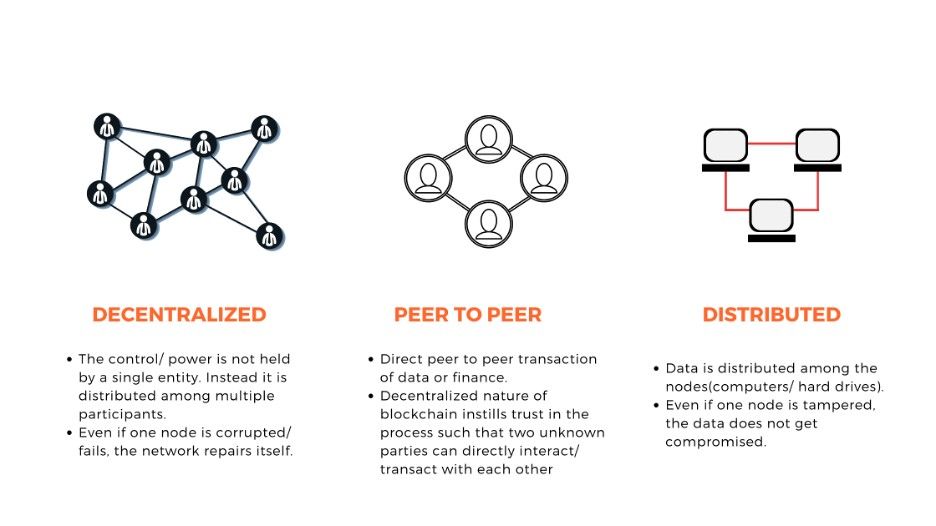

- In Bitcoin’s case, the blockchain is decentralized, so no single person or group has control—instead, all users collectively retain control.

- Decentralized blockchains are immutable, which means that the data entered is irreversible. For Bitcoin, transactions are permanently recorded and viewable to anyone.

How Does a Blockchain Work in Supply Chain?

Blockchain technology can improve supply chain management by providing a secure and transparent way to track goods, reduce fraud, and increase efficiency. Here are some ways blockchain can be used in supply chains:

Security: Blockchain transactions are encrypted with a private key, making them tamper-proof. Multiple copies of transactions are recorded, so any attempt to alter records will be discovered.

Visibility: Blockchain provides real-time visibility of goods as they move through the supply chain. This can help reduce the risk of overstocking or stockouts.

Traceability: Blockchain can be used to track items from origin to destination. For example, Walmart uses blockchain to track the sales of pork in China, including where the meat comes from, processing and storage steps, and sell-by date.

Compliance: Blockchain provides a reliable and auditable record of all transactions and activities, which can help businesses demonstrate compliance with regulations.

Smart contracts: Smart contracts can automatically execute payments at agreed-on milestones, such as delivery of items.

Document management: Blockchain-based file systems assign each document a unique fingerprint, which allows users to identify and track its location, origin, and modification history.

Shared infrastructure: A blockchain's shared IT infrastructure can streamline workflows for all parties in the supply chain.